What FirstCry’s Rs 300 Crore Share Sale In Swara Baby’s IPO Actually Reveals

Swara Baby’s Rs 1,000 crore IPO is being sold as a hygiene manufacturing growth story, but the real headline is that FirstCry’s parent is selling down its stake in a subsidiary growing faster and more profitably than its own listed e-commerce business, and few are asking why.

Highlights:

- Swara Baby has filed DRHP for a Rs 1,000 crore IPO, with FirstCry parent Brainbees Solutions selling Rs 300 crore worth of shares.

- Swara Baby’s revenue grew from Rs 545 crore in FY23 to nearly Rs 943 crore in FY25, with profit rising from Rs 26 crore to Rs 81 crore, a CAGR above 30 percent.

- People familiar with the matter say Brainbees currently holds a 76.59 percent stake, meaning it retains firm control even after the OFS.

- Two people aware of the development said Swara Baby holds over 30 percent market share in India’s contract manufactured diaper segment.

- Neither Swara Baby nor its bankers responded to requests for comment from multiple financial publications ahead of the filing.

There is a specific kind of financial move that gets reported as routine and deserves to be read as revealing, and Brainbees Solutions selling Rs 300 crore worth of its stake in Swara Baby through the subsidiary’s own IPO is exactly that kind of move. The headline write up of this filing focuses, understandably, on the scale of the offering, a Rs 1,000 crore issue split between fresh shares and an offer for sale, and on Swara Baby’s growth story as a diaper and hygiene products manufacturer riding India’s expanding babycare and adult incontinence markets. What gets far less attention is the more pointed question sitting underneath the filing, why is the parent company of one of India’s best known consumer internet brands choosing to partially cash out of a subsidiary that, on the numbers disclosed in the DRHP, looks like the healthier business of the two.

It is worth noting upfront that this is a story built almost entirely on regulatory filings and sourced reporting rather than public statements, because neither Swara Baby nor its investment bankers have said anything on the record. Multiple financial publications, including Business Standard and Business Today, reported that emails sent to the company and to its book running lead managers, JM Financial and Avendus Capital, seeking comment on the IPO plans went unanswered before their stories were filed. That silence is fairly standard practice ahead of a formal listing, companies typically hold public commentary until the DRHP itself is filed and vetted, but it does mean that everything currently known about the transaction’s rationale comes from people familiar with the matter rather than from Swara Baby or Brainbees directly.

Start with what those sources say Swara Baby actually is. Founded in 2016 and led by Managing Director Alok Birla, an industry veteran with over 18 years of experience in the hygiene products sector, the company began in 2021 as a single product operation and has since expanded into seven categories spanning baby pant style and tape style diapers, adult diapers, sanitary napkins and panty liners. It runs four manufacturing facilities in Pithampur and Indore, Madhya Pradesh, and has built supply relationships with global consumer giants including Unicharm, Procter & Gamble, Kimberly-Clark and Kenvue, evidence that its manufacturing quality is trusted well beyond FirstCry’s own retail ecosystem. Two people aware of the development told Business Today that Swara Baby is among the country’s largest contract manufacturers in baby and adult diapers, with a market share of over 30 percent, though they said they were not certain of its exact standing in the sanitary napkins segment. The same sources added that the company’s focus is expected to remain on white labelling for now, with export exposure limited but likely to grow following its recent entry into the US market through a newly incorporated subsidiary, Swara Corp.

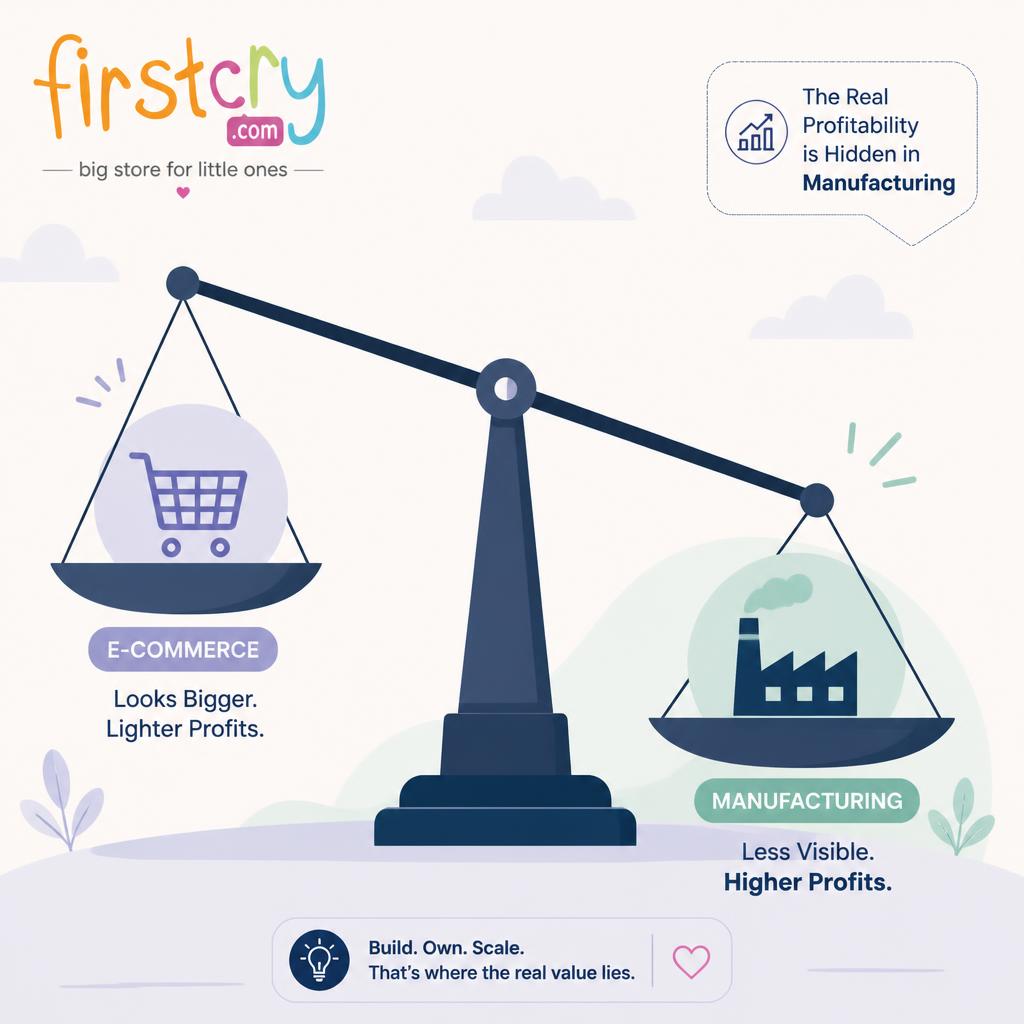

The financial trajectory disclosed in past public filings is the part that should give pause to anyone treating this as a routine IPO. According to figures reported by Business Today and Upstox, Swara Baby posted revenue growth from roughly Rs 545 crore in FY23 to nearly Rs 943 crore in FY25, a compound annual growth rate exceeding 30 percent, while profit after tax rose from Rs 26 crore to Rs 81 crore over the same period, with PAT margins expanding from 4.84 percent to 8.56 percent. That is a growth rate and margin trajectory that most consumer internet businesses in India, FirstCry included, would happily trade for.

That last comparison is the one worth sitting with. Brainbees Solutions, FirstCry’s listed parent, operates a business built primarily on e-commerce and omnichannel retail for baby and kids products, a model that by its nature carries thinner margins, higher logistics costs and constant competitive pressure from marketplaces and quick commerce players encroaching on categories that used to belong to specialised retailers. Swara Baby, by contrast, is a contract manufacturer sitting upstream of all that retail complexity, selling directly into a commodity hygiene products market where it already claims the outsized share described by sources above. Manufacturing businesses in defensible commodity categories with real barriers to entry, BIS certification requirements, established relationships with multinational buyers, dedicated production facilities, tend to be structurally more profitable and more predictable than e-commerce platforms fighting for consumer attention and repeat purchase behaviour every single quarter. The disclosed numbers suggest Swara Baby fits that pattern well.

So why sell down a stake in it now. The most generous reading, consistent with what sources have described, is capital discipline, Brainbees using the OFS proceeds to strengthen its own balance sheet or fund expansion in its core e-commerce business, a perfectly reasonable corporate finance decision that does not require any deeper explanation. Brainbees will still hold a commanding majority after the offering, its current 76.59 percent stake, according to people familiar with the shareholding structure, leaves enormous room to sell Rs 300 crore worth of shares while retaining firm operational control, so this is not an exit in any meaningful sense. But the timing is worth noting regardless, arriving as it does at a moment when Brainbees’ own listed stock has periodically faced analyst scrutiny over the comparatively thin margins in its core e-commerce operations relative to the capital intensity of running warehouses, delivery networks and physical stores across India. Choosing to monetise a portion of its stake in a faster growing, higher margin manufacturing subsidiary right as that subsidiary heads toward a public listing of its own is, at minimum, a signal about where the parent company sees relative value crystallising fastest, even if it is not necessarily a signal of concern about the core business.

There is a second layer to this worth examining, the market Swara Baby is stepping into. Industry estimates cited across multiple reports place India’s diaper market at 1.83 billion dollars in 2025, with projections reaching 3.18 billion dollars by 2034, alongside a rapidly growing adult diaper segment expected to post double digit annual growth through 2030, driven by India’s ageing population and rising awareness around adult incontinence products that were until recently treated as a taboo category. Sources familiar with the company’s plans point to its move to launch a diaper technology reducing conventional wood pulp usage to around 7 percent, reportedly a first for an Indian manufacturer, and its decision to incorporate a US subsidiary to expand international diaper trading, as evidence that Swara Baby is positioning itself for a growth runway well beyond simply supplying FirstCry’s own retail shelves.

None of this necessarily means investors should read the OFS as a red flag about FirstCry’s broader health, Brainbees remains the dominant shareholder and stands to benefit enormously from any value creation Swara Baby delivers as a public company, particularly given the scale of stake it continues to hold. But the framing that has dominated coverage of this filing so far, a straightforward growth story about a hygiene products manufacturer going public, misses the more interesting tension actually sitting inside the numbers. A parent company built on a lower margin, capital intensive e-commerce model is monetising a portion of its stake in a subsidiary that has, by the disclosed figures, grown revenue and nearly tripled profit over two years while operating in a structurally more defensible category. That is not evidence of anything going wrong at FirstCry. It is, however, a reminder that sometimes the most profitable part of a well known consumer brand is not the part carrying its name on the app icon, and that investors evaluating this IPO should be asking not just whether Swara Baby is a good business, which the numbers suggest it is, but what it says about capital allocation priorities inside the broader Brainbees group that this particular business is the one being partially monetised first.